The “Little Carpathians” of Slovakia, a range of rolling hills near Bratislava, have become the unlikely ground zero for a geopolitical tug-of-war. Within these woods lies the Trojarova project, a Cold War-era mine once mapped by Soviet engineers, now owned by Canada’s Military Metals Corp (CSE: MILI). As the European Union struggles to reconcile its lofty green and defense ambitions with a fragmented industrial reality, Trojarova serves as a “litmus test” for the entire EU’s ability to break its near-total reliance on China for antimony—a critical metalloid essential for everything from munitions to solar panels.

Despite the strategic stakes, the EU remains caught in a cycle of “ambition without execution”. While the United States has moved aggressively to fund domestic projects, such as the $180 million in combined grants awarded to Perpetua Resources in Idaho, European projects like Trojarova are often left to languish without the offtake agreements or direct state financing required to reach production.

“What we are still lacking is not ambition, but execution,” noted Thomas Hüser, Chairman of Military Metals and former Glencore manager. Without a unified strategy, Europe risks losing these critical assets to rivals who move faster and with greater financial clarity.

In April 2026, Military Metals reported a landmark maiden Inferred Mineral Resource for Trojarova, containing approximately 67,000 tonnes of antimony and 222,000 ounces of gold. This makes it the largest antimony resource in the EU defined by modern regulatory standards. At a projected output of 6,000 tonnes per year, a single facility at Trojarova could potentially meet one-third of Europe’s total annual demand.

Yet, even with these numbers, Military Metals’ CEO Scott Eldridge has highlighted the uphill battle: “Europe needs its own supply, but the financing mechanisms aren’t there yet to compete with the US or China”.

An Antimony Primer – Supply and Demand

Antimony is often called the “Great War Metal” due to its historical and modern-day military applications, but its role in the global energy transition has recently sent prices to record highs.

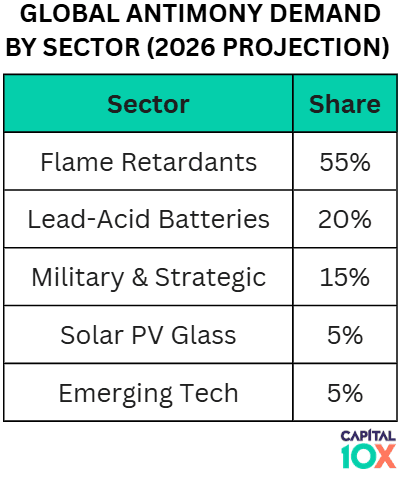

1. Where is it Used? (Demand Split)

Antimony’s demand is dominated by three primary sectors:

Source: USGS.com, Fastmarkets.com

- Flame Retardants (~60%): Antimony trioxide (ATO) is used in plastics, textiles, and electronics to prevent the spread of fire. This remains the largest single market, driven by global safety regulations.

- Lead-Acid Batteries & Alloys (~25%): It acts as a hardening agent in lead-acid batteries, which are critical for automotive starters and backup power systems in data centers.

- Strategic & Emerging Tech (~15%): This includes military uses (ammunition and infrared sensors), solar PV glass (clarifiers), and high-end electronics.

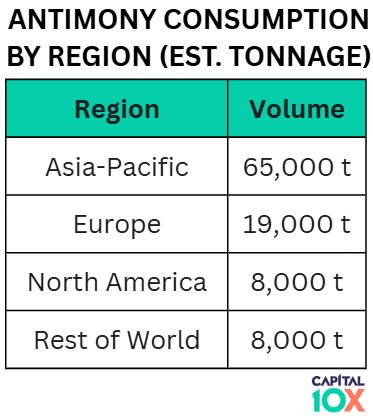

2. Regional Consumption: The Great Disparity

Consumption is heavily concentrated in manufacturing hubs, with Asia leading by a wide margin.

Source: USGS.com, Fastmarkets.com

- Asia-Pacific: Accounts for approximately 64-68% of global demand, fueled by China’s massive electronics and polymer industries.

- Europe: Consumes roughly 18-20% of the global supply (approx. 24,000 metric tons/year), primarily for specialty chemicals and defense.

- North America: Represents about 7-8% of demand but is nearly 90% dependent on imports, particularly for defense-grade material.

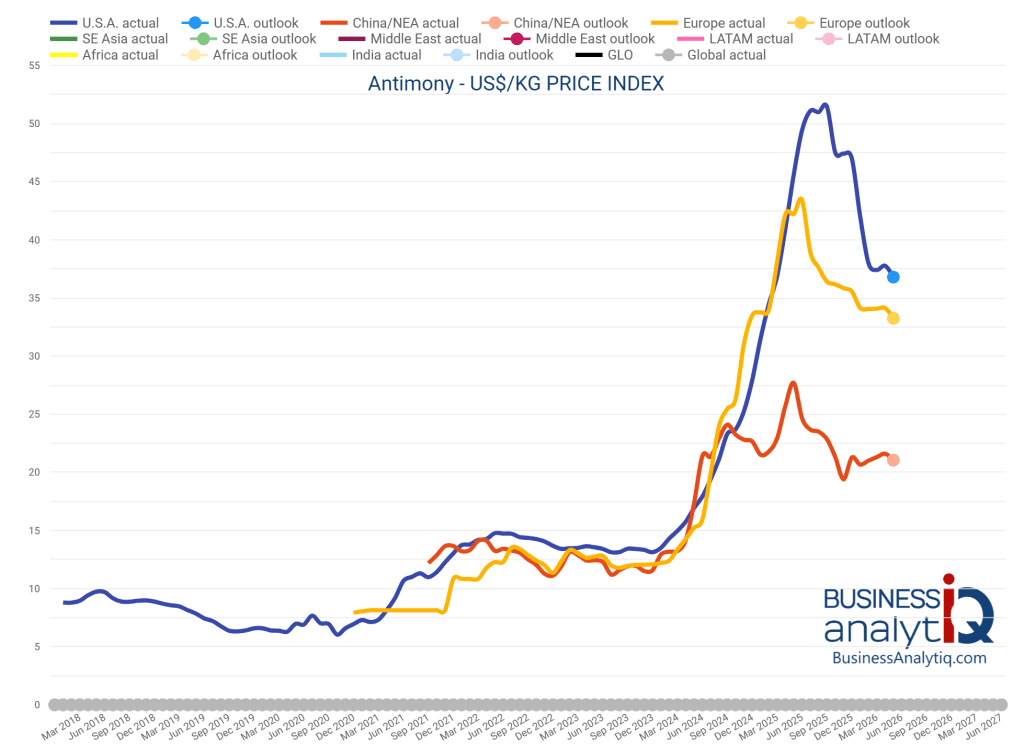

3. Supply Constraints and Geopolitics

The global supply of antimony is exceptionally concentrated. In 2025, China, Russia, and Tajikistan accounted for over 80% of global mine production. China’s decision in late 2024 to impose strict export controls—and a subsequent ban on exports to the U.S. in December 2024—sent global prices skyrocketing from $5.60/lb to over $25.00/lb by mid-2025. This supply “chokehold” has forced Western governments to treat antimony projects as matters of national security, placing companies like Military Metals at the center of a new industrial frontline.

Antimony Prices

4. Emerging Sources of Demand and the Global Corporate Landscape

The resurgence of antimony in 2026 is not merely a byproduct of defense anxiety; it is being propelled by a fundamental shift in high-tech industrial needs. While traditional uses in flame retardants remain the bedrock of the market, a “Second Wave” of demand is emerging from the heart of the global energy transition and digital infrastructure.

5. Emerging Sources of Demand – Solar, AI and Battery Storage

The most significant new driver is the photovoltaic (PV) solar sector. Sodium antimonate is increasingly utilized as a glass clarifier in high-efficiency solar panels. It reduces melting temperatures during manufacturing and improves light transmission, which is critical for maximizing energy yield. In 2025, global PV installations reached nearly 280GW, and as the industry moves toward 2030 targets, this “rigid demand” has become a permanent fixture of the antimony market.

Furthermore, the data center boom—driven by the rapid expansion of Artificial Intelligence—has created a secondary demand surge. Thousands of miles of high-capacity fiber and copper cabling required for these facilities use antimony trioxide (ATO) in their PVC coatings to meet stringent fire safety standards. Finally, the next generation of liquid metal and molten salt batteries for long-duration grid storage is beginning to move from pilot to commercial scale. These batteries use an antimony-magnesium or antimony-lead chemistry that is non-flammable and capable of thousands of charge cycles, positioning the metal as a potential rival to lithium in stationary storage.

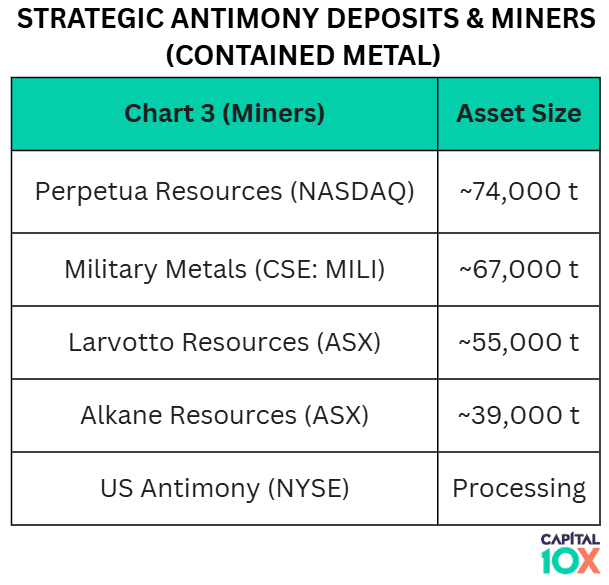

6. Publicly Traded Antimony Miners and Strategic Deposits

As supply from China and Russia remains restricted, a handful of Western-listed companies have emerged as the “New Guard” of antimony production.

Source: Company Filings, Capital10x Estimates, Bloomberg

• Military Metals Corp (CSE: MILI / OTCQB: MILIF): Headquartered in Canada, Military Metals is the primary player in Europe. Its flagship Trojarova project in Slovakia holds a maiden Inferred Resource of 67,000 tonnes of antimony, making it the largest compliant resource in the EU. The company’s strategic focus is on providing a localized, non-Chinese source for the European defense and energy sectors.

• Perpetua Resources (NASDAQ: PPTA): The leading U.S. contender, Perpetua is advancing the Stibnite Gold Project in Idaho. Backed by over $1.8 billion in proposed federal loan support, it aims to be the only domestic producer of antimony trisulfide for the U.S. military. A final investment decision is expected in the second half of 2026.

• Larvotto Resources (ASX: LRV): Australia’s premier antimony play, Larvotto is on track to restart the Hillgrove Mine in New South Wales in August 2026. Once operational, it is expected to provide approximately 7% of the world’s antimony supply, effectively becoming the largest producer in the Western world.

• Alkane Resources (ASX: ALK): Following its 2025 merger with Mandalay Resources, Alkane operates the Costerfield Mine in Victoria, Australia. Costerfield is a consistent producer of high-grade antimony-gold concentrate, with an annual output of roughly 1,300 to 2,800 tonnes.

• United States Antimony Corp (NYSE: UAMY): A veteran of the sector, UAMY is the only integrated antimony miner and smelter in the U.S. It manages a diverse portfolio of sourcing and processing facilities and has set a revenue target of $125 million for 2026.

• Antimony Resources Corp (CSE: ATMY): A Canadian junior focused on the Bald Hill project in New Brunswick. Recent 2026 drilling has uncovered one of the world’s highest-grade deposits, with conceptual targets of up to 100,000 tonnes of contained metal.

• NevGold (TSXV: NAU): Focusing on the Limousine Butte project in Nevada, NevGold is targeting a maiden resource estimate in Q2 2026, utilizing historical heap leach pads for near-term production potential.

Antimony Will Continue to be the Main Beneficiary of a reshoring of western critical minerals supply

The convergence of military necessity, energy transition demand, and geopolitical supply disruption has transformed antimony from an obscure industrial metalloid into one of the most strategically consequential commodities of the 2020s.

China’s export restrictions have exposed a critical vulnerability in Western supply chains that years of complacency helped create, and the scramble to fill that gap — from the hills of Slovakia to the mountains of Idaho to the mines of New South Wales — is now very much underway.

Yet despite the urgency, Western-listed antimony producers and developers remain significantly undervalued relative to the scale of the problem they are positioned to solve. While antimony prices have surged from roughly $6.00 per pound in 2023 to over $17.00 per pound in 2026, the market capitalizations of companies like Military Metals, Perpetua Resources, Larvotto, and peers have not kept pace with either the commodity’s price appreciation or the strategic premium that governments are increasingly willing to assign to secure, non-Chinese supply.

As offtake agreements solidify, permitting advances, and financing mechanisms catch up with political will, the re-rating of these assets toward their true strategic value is likely.