Why forced selling may create a rare opportunity for long-term outperformance

Executive summary

Every so often, passive funds create opportunities not because fundamentals change, but because rules change. The Sprott Uranium Miners ETF (URNM) is approaching one of those moments.

On Friday, December 19, URNM will rebalance under new index methodology rules that explicitly remove companies with a free-float market capitalization below $100 million. As a result, several smaller uranium developers are expected to be fully sold out of the ETF, including Anfield Energy.

History suggests that this kind of forced selling can matter. A large body of empirical research shows that stocks removed from indexes or passive ETFs often outperform the market over the subsequent five years, not because they suddenly improve, but because mechanical selling temporarily depresses prices below intrinsic value.

We argues that Anfield Energy represents one of the more compelling examples of this setup:

- It faces material forced selling pressure from URNM relative to its trading liquidity.

- It has already underperformed URNM meaningfully since the deletion was announced.

- It trades at a deep valuation discount to uranium peers on both resource and NPV metrics.

- It has tangible, time-bound operational catalysts tied to U.S. uranium production and mill restart optionality.

Taken together, the evidence supports the conclusion that buying Anfield Energy before, during, or shortly after its removal from URNM could offer attractive long-term outperformance potential, particularly for investors with a multi-year horizon.

1. What history tells us about index deletions

Forced selling is real—and it distorts prices

Academic research on index rebalancing consistently finds that index deletions are not neutral events. When a stock is removed from an index:

- Passive funds tracking that index must sell, regardless of valuation.

- That selling is price insensitive and often concentrated around the rebalance date.

- The result is a temporary liquidity shock, not a reassessment of fundamentals.

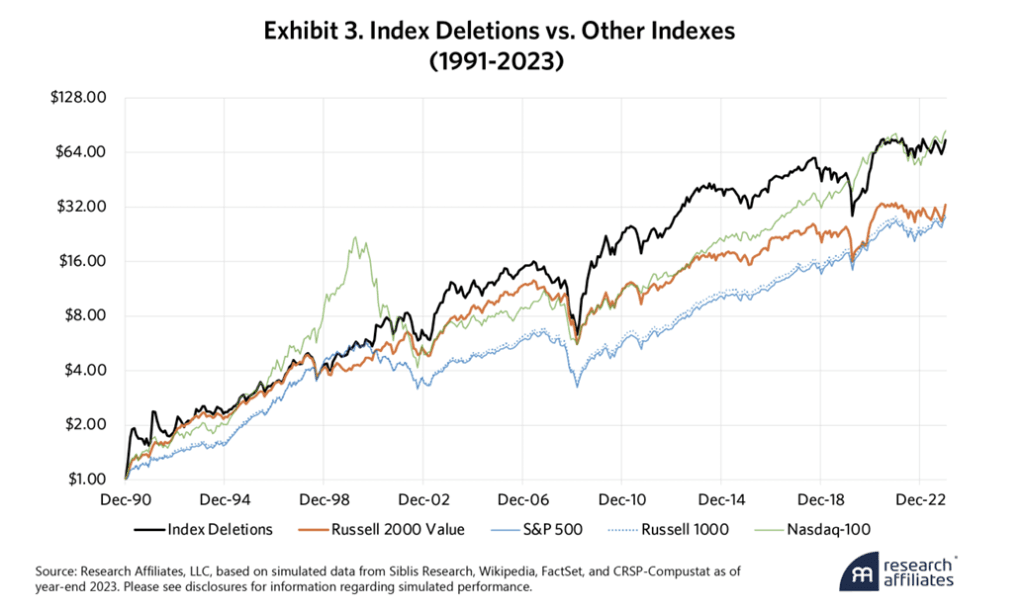

Research Affiliates’ long-running work on index deletions provides a clear framework for understanding the opportunity this creates.

Stocks kicked out of indexes have historically outperformed

According to the Research Affiliates study:

- Stocks removed from major U.S. equity indexes outperformed their benchmarks for at least five years after deletion.

- The average excess return exceeded 5% per year, compounded over the five-year post-deletion period.

- This outperformance persisted across multiple market cycles and index families.

Importantly, the research emphasizes that:

- Most deletions underperform sharply in the year leading up to removal, as selling pressure builds.

- The rebound typically occurs after the forced selling ends, once marginal sellers disappear.

This pattern matters because it closely resembles what is currently happening in URNM’s smaller holdings.

The lesson: timing matters, but patience matters more

Two important caveats from the research apply directly here:

- Deletions are volatile. Prices do not necessarily bottom on the rebalance day itself.

- Dispersion is wide. Not every deleted stock becomes a winner, which is why basket strategies often outperform single-name bets.

That said, when a deleted stock is:

- fundamentally viable,

- trading at a valuation extreme,

- and subject to outsized forced selling,

the odds of mean reversion over a multi-year period improve meaningfully. URNM is likely to remove

2. What is happening at URNM on December 19

A meaningful change in index methodology

In 2025, Sprott announced material changes to the North Shore Global Uranium Mining Index, which URNM tracks. The most important change for investors is the introduction of much higher size and liquidity thresholds.

Key rule changes include:

- Minimum free-float market cap

- New constituents: $125 million

- Existing constituents (buffer): $100 million

- Minimum liquidity (ADVT)

- New constituents: $100,000

- Existing buffer: $75,000

- Removal of minimum weight constraints, allowing small names to be fully eliminated

- Higher concentration caps for larger holdings

These changes explicitly bias the index toward larger, more liquid uranium companies and away from smaller developers. Essentially URNM is cutting out small caps from the index and upping exposure to the largest uranium stock in the market, Cameco. We question if this is what investors really wanted.

Expected Deletions from URNM

Based on Sprott’s published pro-forma illustrations, the following companies are expected to be fully removed from URNM at the December rebalance:

- Forsys Metals (FSY CN)

- Premier American Uranium (PUR CN)

- Alligator Energy (AGE AU)

- Elevate Uranium (EL8 AU)

- Berkeley Energia (BKY LN)

- Western Uranium & Vanadium (WUC CN)

- Skyharbour Resources (SYH CN)

- Atomic Eagle (AEU AU)

- Anfield Energy (AEC US)

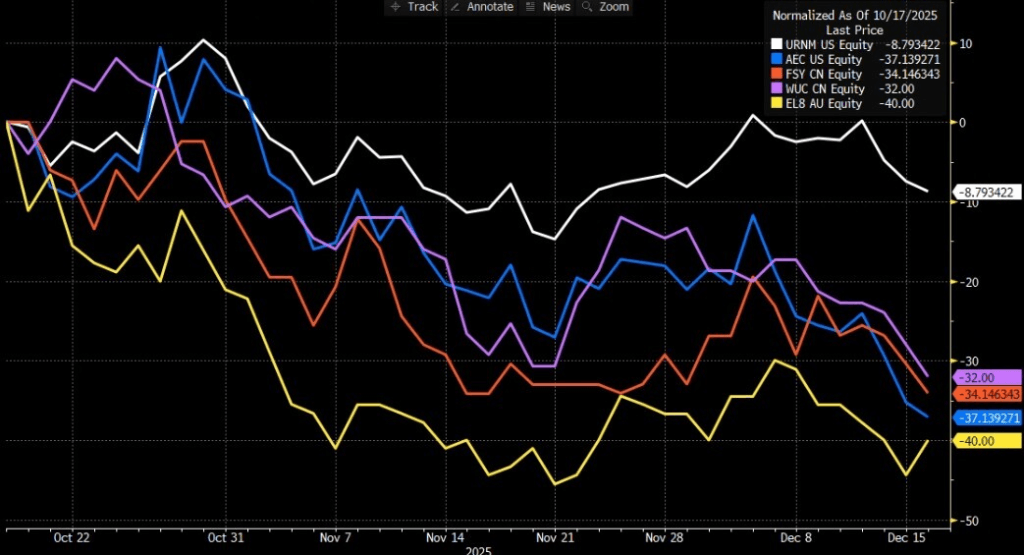

While Sprott notes that final constituents are subject to confirmation, the direction of travel is clear: sub-$100M companies are being pushed out by design. Looking at the performance of four specific smaller holdings in URNM since the rebalancing was announced, its clear these stocks are under pressure. Significantly underperforming URNM and the uranium price.

Price performance Small Holdings in URNM from 10/17 to today

3. Toro Energy: a real-world example of forced selling and recovery

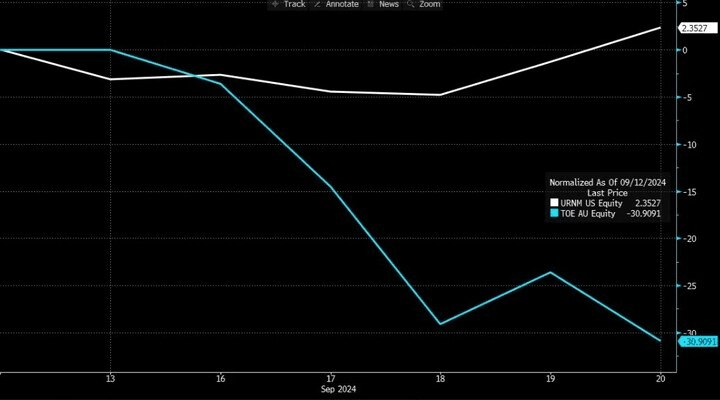

To understand how this dynamic can play out in practice, it is useful to look at Toro Energy, a uranium developer that was previously removed from URNM in 2024.

Before deletion: severe underperformance

In the period leading up to its deletion:

- Toro Energy underperformed URNM by over 30 percentage points on a normalized basis.

- The stock declined sharply while URNM remained relatively stable.

This mirrors the pattern described in the academic research: selling pressure accumulates well before the rebalance date.

Toro Energy % Return vs URNM: Rebalance Announcement Date until T-1 to Rebalance

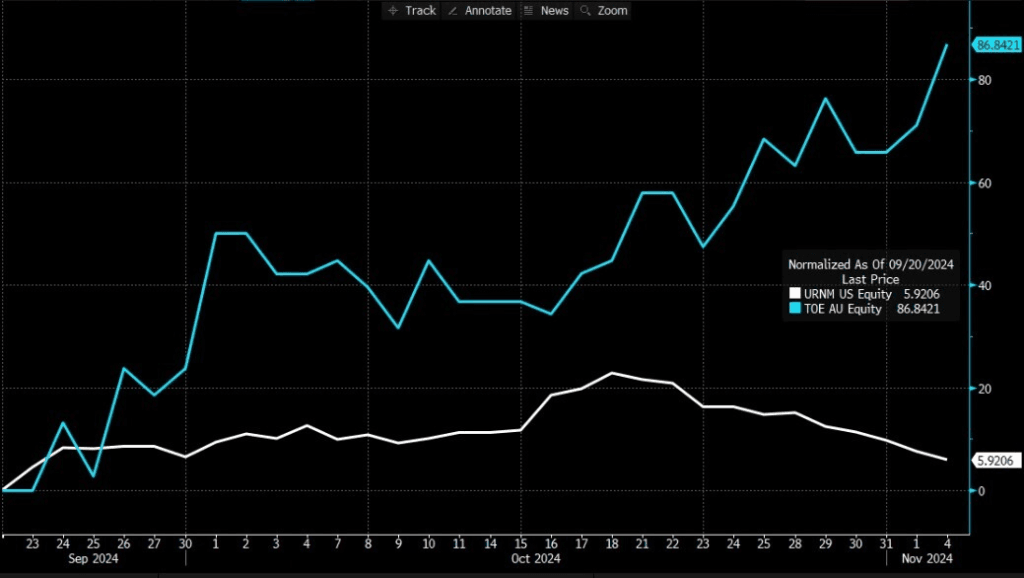

After deletion: sharp relative rebound

In the period following removal:

- Toro Energy dramatically outperformed URNM, rising 86% compared to only a 6% return for URNM in the following month.

- The rebound occurred after the forced selling ended and liquidity normalized.

Toro does not prove that all deletions succeed. However, it does demonstrate:

- How passive selling can overwhelm price discovery, and

- How relief from that selling can unlock rapid mean reversion.

We believe this historical precedent is directly relevant to Anfield Energy today.

4. Anfield Energy: flows, performance, and near-term pressure

Underperformance since the deletion announcement

Since mid-October, stocks scheduled for deletion from URNM have meaningfully underperformed the ETF itself.

Across the deletion cohort:

- URNM declined less than 10%.

- Several deletion candidates fell 30–40% over the same window.

This pattern strongly suggests that:

- Markets are front-running the rebalance, and

- Forced selling pressure is already being reflected in prices.

Anfield has participated in this broader underperformance dynamic even though it has several concrete catalysts coming up in the next 18 months plus trades at a significant valuation gap to other uranium explorers and developers.

URNM’s ownership of Anfield is large relative to liquidity

The most important quantitative detail for Anfield is the scale of URNM’s ownership versus daily trading volume.

Based on holdings data from URNM as of December 16th:

- URNM holds approximately US$6.25 million of Anfield stock.

- Anfield trades roughly US$430,000 per day in dollar volume.

- This implies URNM’s position equals ~14.5 days of normal trading volume.

This is significant.

We would note that ETF’s usually do larger trades as a block with a pre-arranged party. This avoids the type of mass price declines open market selling would cause on the rebalance day. However the front running by market participants is real and coupled with the ETF selling, almost always puts downward pressure on positions schedule for deletion. This price pressure has happened to

What happens if URNM sells?

While ETFs do not necessarily dump shares via simple market orders, the reality is unavoidable:

- Those shares must change hands.

- A sale equivalent to two weeks of volume is likely to pressure the price, especially in thin markets.

The most likely outcomes are:

- Weakness into today’s close on December 19.

- Possible spillover selling into Monday, December 22, if liquidity is insufficient.

- Heightened volatility around the rebalance window.

Crucially, however, this selling is non-fundamental. Once it is complete, the marginal seller disappears.

5. Anfield’s fundamentals and valuation asymmetry

Strategic positioning: U.S. uranium infrastructure

Anfield’s strategy is centered on becoming a U.S.-focused uranium producer, anchored by ownership of the Shootaring Canyon Mill, one of only three constructed and permitted hard rock uranium mills mills in the United States.

This infrastructure optionality matters in a market increasingly focused on:

- Domestic uranium supply,

- Energy security,

- And permitting-constrained assets.

Operational timeline and catalysts

Key milestones include:

- Velvet-Wood project (Utah)

- State and federal approvals in place.

- Approved to advance toward construction.

- JD-8 mine (Colorado)

- Permitting application submitted.

- Management targeting restart in the second half of 2026.

- Shootaring Canyon Mill

- Radioactive materials license expected in 2H 2026.

- Restart of the mill planned for 2027 with a goal of 3M lbs of uranium produced annually.

While not risk-free, these are defined, observable catalysts that could drive a future rebound in Anfield shares.

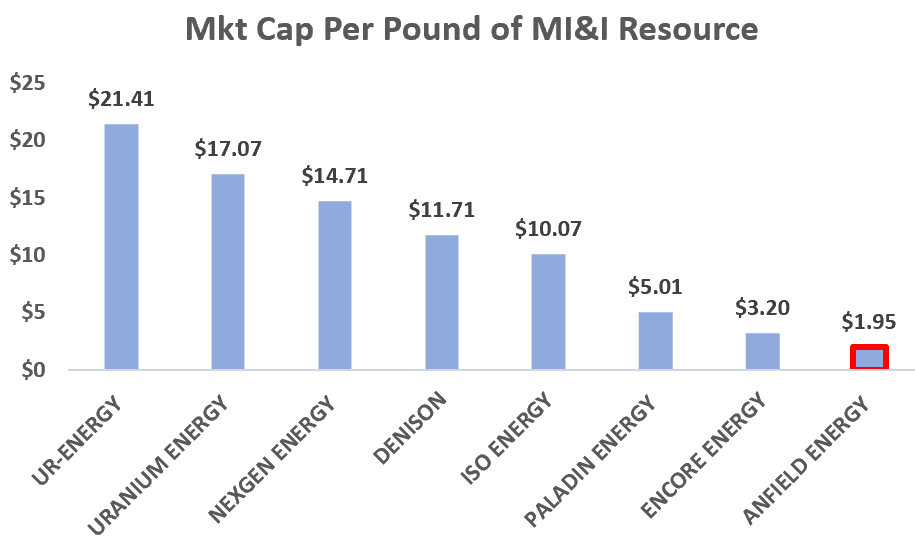

Anfield also has Significant Valuation Support

On multiple valuation measures, Anfield screens as one of the cheapest uranium developers in the public market.

- Market cap per pound of M&I resource

- Anfield trades at roughly $1.95 per pound, the lowest among peers.

- Most peers trade between $5 and $20+ per pound.

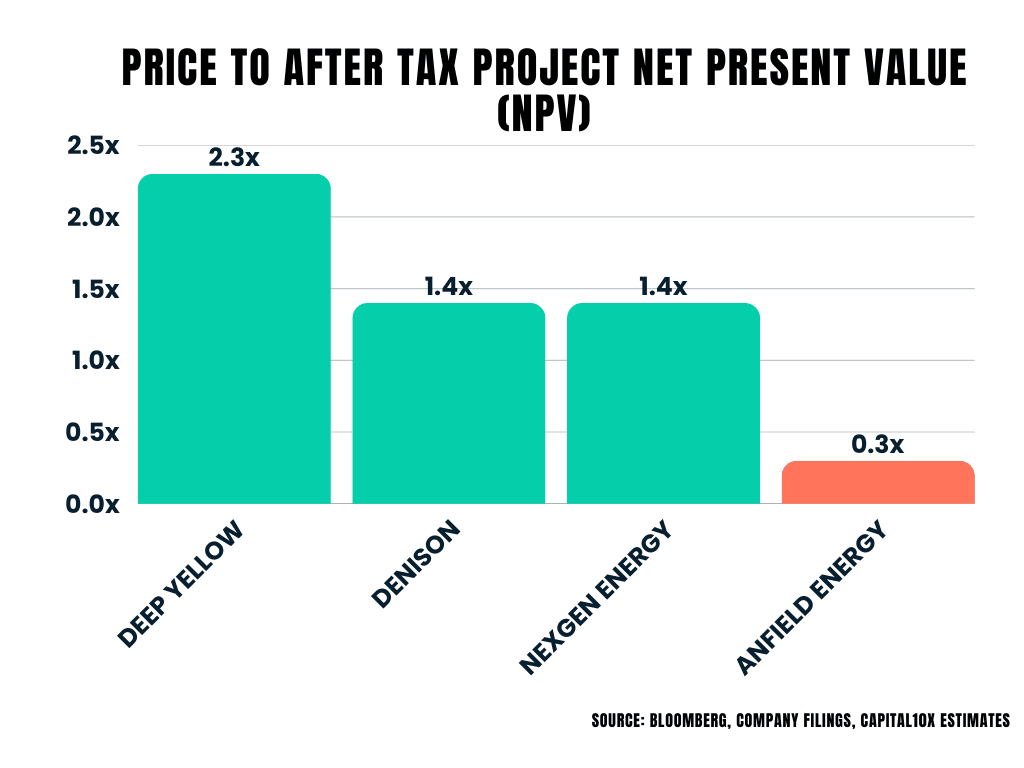

- Price to after-tax project NPV

- Anfield trades near 0.3× NPV.

- Major developers on similar timelines to first production trade between 1.4× and 2.3× NPV.

These gaps reflect execution risk—but they also create asymmetric upside if even modest progress is made.

Given the Fundamental Backdrop for Uranium: Buying Index Deletions Could be a Smart Strategy

The case for Anfield around the URNM rebalance is not based on hope, hype, or short-term trading finesse. It is based on structure.

- A large passive ETF must sell.

- The sale is large relative to liquidity.

- The stock has already underperformed in anticipation.

- The company trades at deep valuation discounts.

- And it has real assets and identifiable catalysts.

History these ingredients drive significant outperformance vs the index.

In our view, investors who are willing to tolerate near-term volatility and focus on a 1-2 year horizon, buying Anfield Energy or potentially all of the URNM deletion candidates before or shortly after their removal from URNM could prove rewarding, particularly if the forced selling creates prices disconnected from fundamentals.