The Green Industrial Revolution

Capital 10X launches our new series ‘Green Metals in Focus’ to help investors understand the foundational metals of the green economy.

The green industrial revolution is here, driven by consumer demand for greener technologies. The key drivers of green technological change are:

- Fuel efficiency

- Battery storage

- Electric vehicles

- Renewable power

Capital markets have consistently underappreciated the fact that metals are the foundation of the green economy. These “green” metals include: copper, cobalt, lithium, vanadium and rare earth metals.

We begin the Green Metals in Focus series with vanadium. Vanadium not only increases efficiencies and adds value to a number of manufacturing processes, but is also considered a foundational element of the “green” industrial revolution.

Vanadium – The Strategic Green Metal

For our readers unfamiliar with this resource Vanadium is a silver/grey malleable metallic element, derived from minerals and used mainly to form alloys (e.g. steel) and as a catalyst for chemical reactions.

Although Vanadium (as an element) is not considered rare as it is abundant on the earth’s crust, it is quite rare in its metallic form. Its value-add to industrial manufacturing has made it a mainstay and in-demand resource over the past decade.

Vanadium is considered a strategic green metal, its key green applications include:

- Increased steel efficiency and strength

- Improved aircraft fuel efficiency

- Vanadium redox flow batteries

Steel Efficiency

Investors in vanadium-related industries note that the most well-known and profitable application for this resource is in the production of steel, rebar, and other building materials.

In fact, 1 pound of ferro-vanadium added to 1 tonne of steel nearly doubles its strength, making it a sought-after material for inclusion in construction projects.

Ferro-Vanadium’s anti-corrosive and tensile properties makes it a go-to resource in China with 84% of producers using Vanadium micro-alloying to strengthen their rebar.

Automobiles

One of the key steel applications for vanadium is in automotive. There was practically no Vanadium used in the automobile industry 20 years ago. Today that has increased to 45%.

By 2025 it is estimated that 85% of all cars will be built with Vanadium alloy – reducing the overall weight and increasing fuel efficiency – thus adhering to stringent EPA standards. Investors should find it of interest that industrial production is now a leader in the green energy revolution.

Aerospace

In aerospace, Titanium-Aluminum-Vanadium (Ti-Al-V) alloy producers are the largest consumers of Vanadium outside of the steel industry with substantial growth in the marketplace.

A layer of vanadium is used to bond titanium and steel for aerospace applications. These alloys are essential for the manufacture fuel-efficient aircraft, with no available substitutes without sacrificing performance.

Batteries

One of the applications of vanadium with significant potential upside is the vanadium redox flow battery used for grid energy storage. With a smaller carbon footprint, and a longer battery life the growth potential for industrial production is high.

While lithium-ion batteries are common place for consumer applications (electronics and electric vehicles), utility-scale Li-ion batteries are rare. Vanadium flow batteries are considered safer and longer-lasting for utility scale applications versus any other battery technology.

Vanadium flow batteries are nonflammable, compact, reusable over semi-infinite cycles, discharge 100% of the stored energy and do not degrade for more than 20 years.

As renewable power becomes a greater component of electricity production globally there will be a increased need for grid energy story – the vanadium redox flow battery is one of the leading technologies in this area.

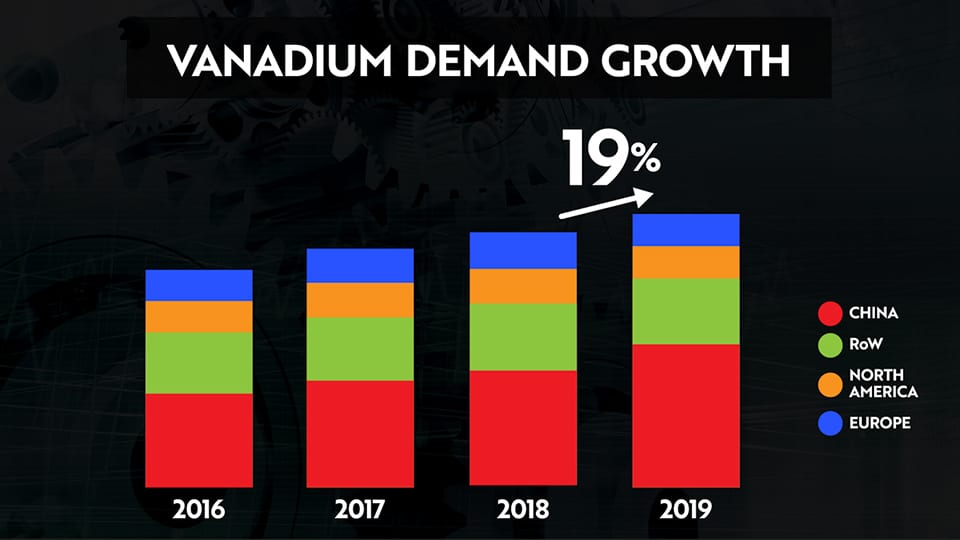

Strong Structural Demand Growth

Over the last decade there has been strong industrial demand for vanadium, driven primarily by the Chinese steel sector and rebar production.

Data reveals that there has been little to no impact to China’s steel sector in the wake of the COVID-19 pandemic. In fact, in May 2020, the Chinese government revealed a fiscal stimulus package of approximately $506 billion US, which is anticipated to drive further demands for infrastructure projects and vanadium demand growth.

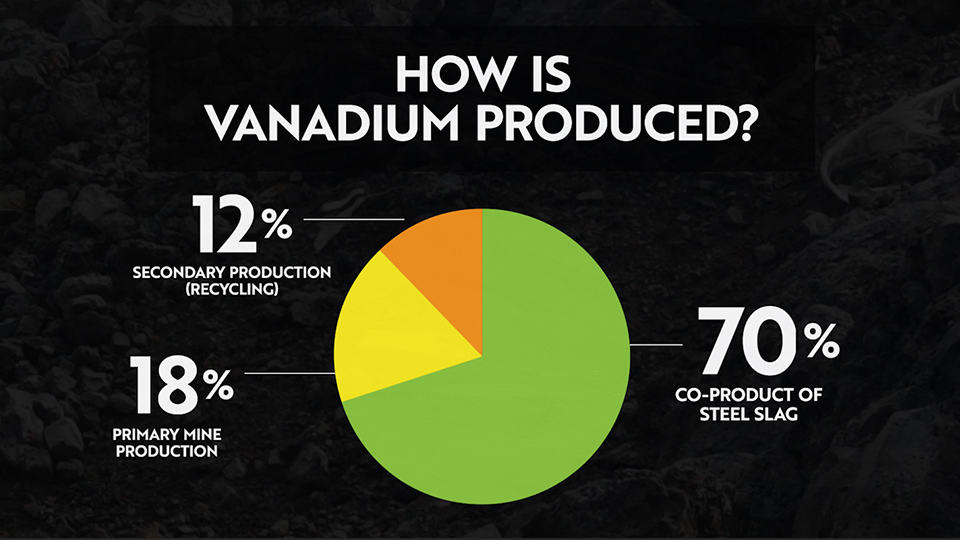

How is it Produced?

Vanadium is produced primarily through a co-product of steel slag, it represents 70% of total output and is higher cost. Primary mine production, the lowest cost, only represents 18% of production.

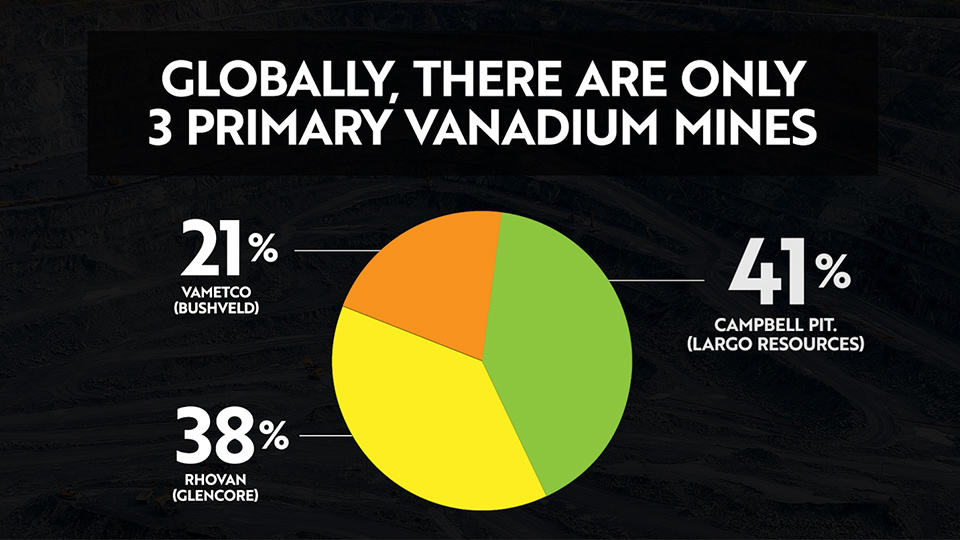

Primary Vanadium Mine Production & Cost

Globally there are only three primary vanadium mines:

- Campbell Pit (owned by Largo Resources)

- Vametco (owned by Bushveld)

- Rhovan (owned by Glencore)

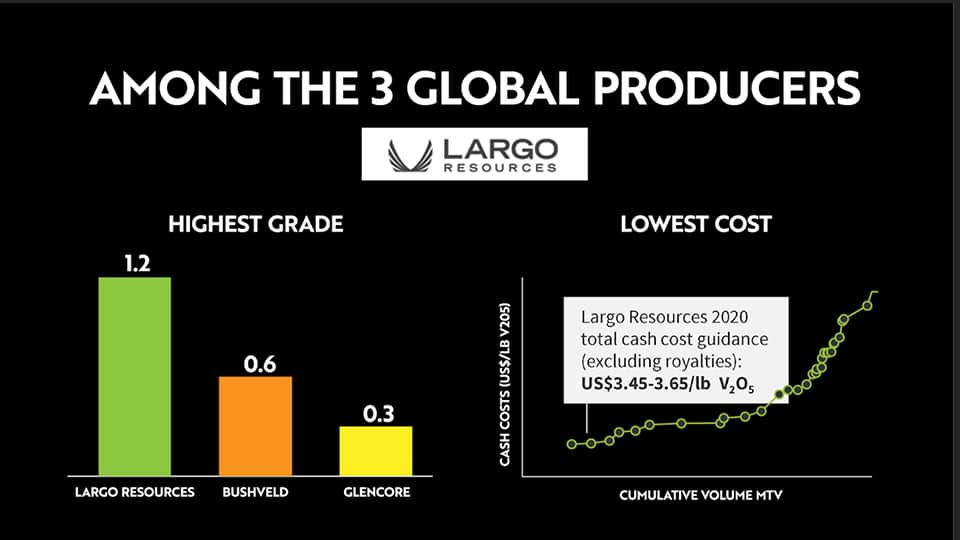

Among the three global producers Largo Resources (TSE:LGO) has highest vanadium head grade and concentrate grade. Largo Resources head grade is 1.2% V205, double that of the next closest mine (Bushveld at 0.6% V205).

The high mining grades for Largo Resources translates to a very attractive cost positioning versus the global vanadium industry. The company is firmly in the first quartile of production cash cost within the industry at US$3.45-3.65/lb V205.

Vanadium – A Key Metal in the Green Industrial Revolution

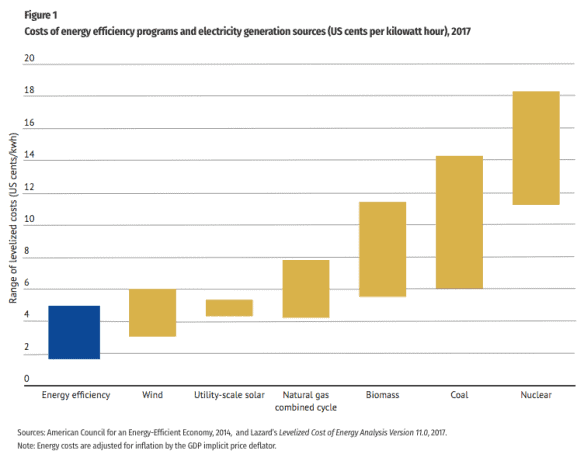

Energy efficiency has always been one of the most cost effective ways to “green” the economy, the chart below highlights the significant cost advantage of energy efficiency versus various forms of electricity generation.

Costs: Energy Efficiency vs. Electricity Generation Sources

Vanadium is the ‘efficiency metal’ and arguably one of the most strategic green metals in the economy; driving resource efficiency, fuel efficiency and battery technology.

Largo Resources is a market awareness client of Capital 10X.

Largo Inc. is a market awareness client of Capital 10X.