The modern royalty company was birthed in 1986 with Franco-Nevada’s conversion from an explorer into a royalty.

Fast forward to today and the royalty industry is now more than 35 companies worth $66 billion of market value, exeeding the value of the entire junior mining industry.

The royalty industry has demonstrated it can generate value over decades.

Even though the industry has exploded in popularity and value over the past three decades, individual investors and small advisors still think of mining exposure primarily through publicly traded explorers, not royalties.

This is a mistake.

History has shown that a well diversified mining portfolio with explorers and royalties generates superior risk adjusted returns over time.

To help anyone not familiar with the royalty business model understand its value, we’ve put together a comprehensive primer on all things royalties.

Royalty economics, key differences, how to find quality royalty operators and three interesting ideas to get you started.

The Funding Landscape Has Changed In Favor of Royalties

A fundamental shift is taking place across the fundraising landscape, with important implications for royalty investors.

20 years ago, active asset managers provided the incremental dollar to mining companies. They had dozens of analysts poring over drill assay’s and providing the capital for each company to move through the riskiest stages of a mine’s life: funding, permitting and construction.

Today these same investment groups are a shadow of what they once were. We’ve seen 10 years of asset outflows and the analyst teams are down to one or two people and marching orders from management to hug the benchmark, not step outside the box for underfollowed small-cap opportunities.

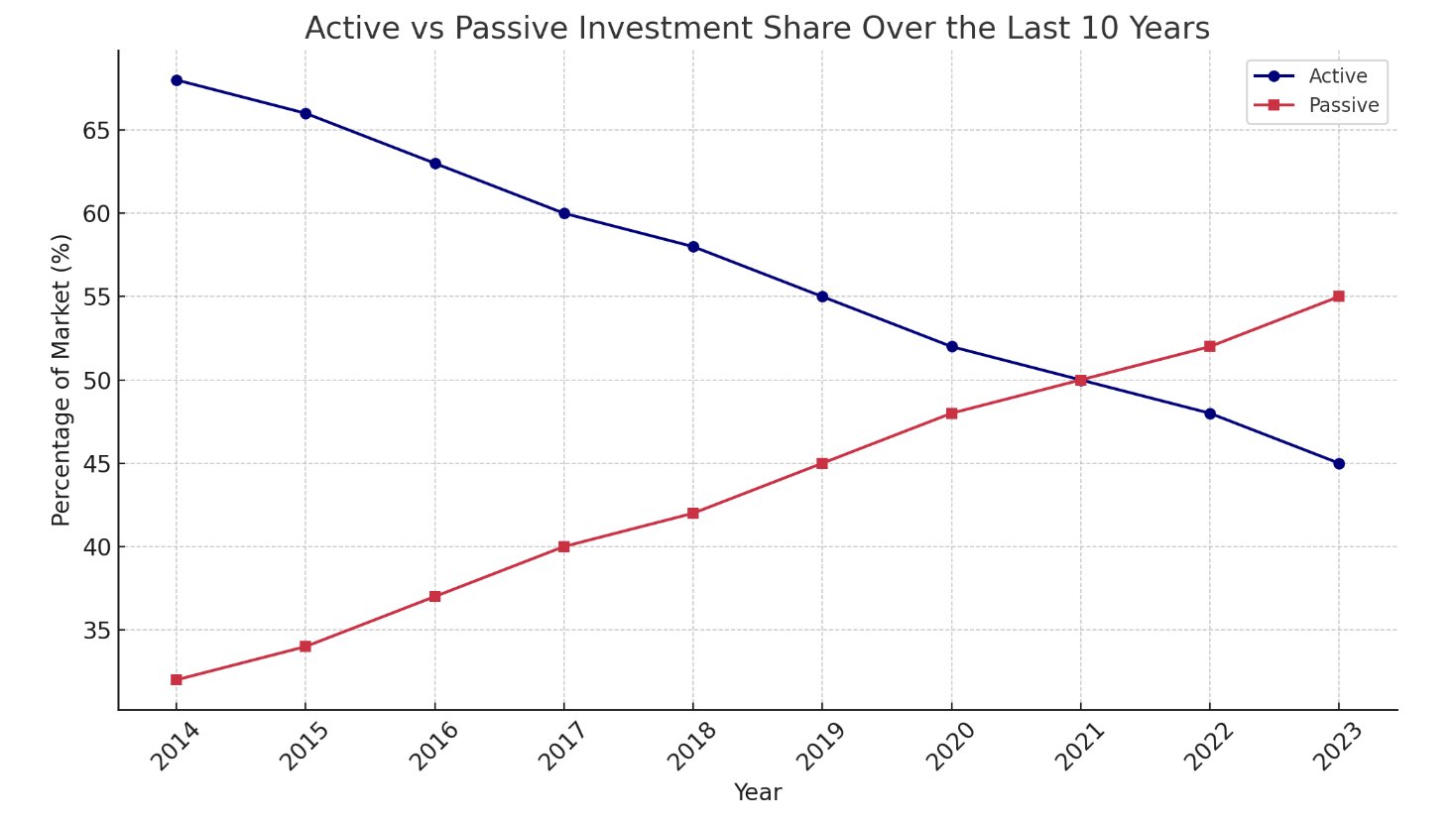

Money is Flooding into Passive Portfolios at the Expense of Active Funds

As a result, passive ETF’s now control more of the market than once dominant active managers.

As a result, passive ETF’s now control more of the market than once dominant active managers.

Explorers and developers across the commodity spectrum now find themselves scrambling to find capital with passive funds no longer participating in most private capital raises.

Royalty companies and high net worth investors have now become the major source of funding in the mining industry

The lack of competition for funding has created an important opportunity for royalty companies to step into the void and generate even better returns than they ever have.

Investors who own mining companies but have never looked at royalty companies are missing out on potentially the best risk adjusted return option in the mining industry.

So What is a Royalty?

A royalty is an interest in the ultimate production of a mine. Royalties differ from owning an entire mining company in that the royalty owner usually gets paid directly from selling the output of the mine, before any operating costs are factored in. This is a huge advantage for the royalty owner.

The one advantage to owning a mining stock over a royalty is the mining stock owns the economics of 100% of the property while a royalty is sometimes on only a portion of the property.

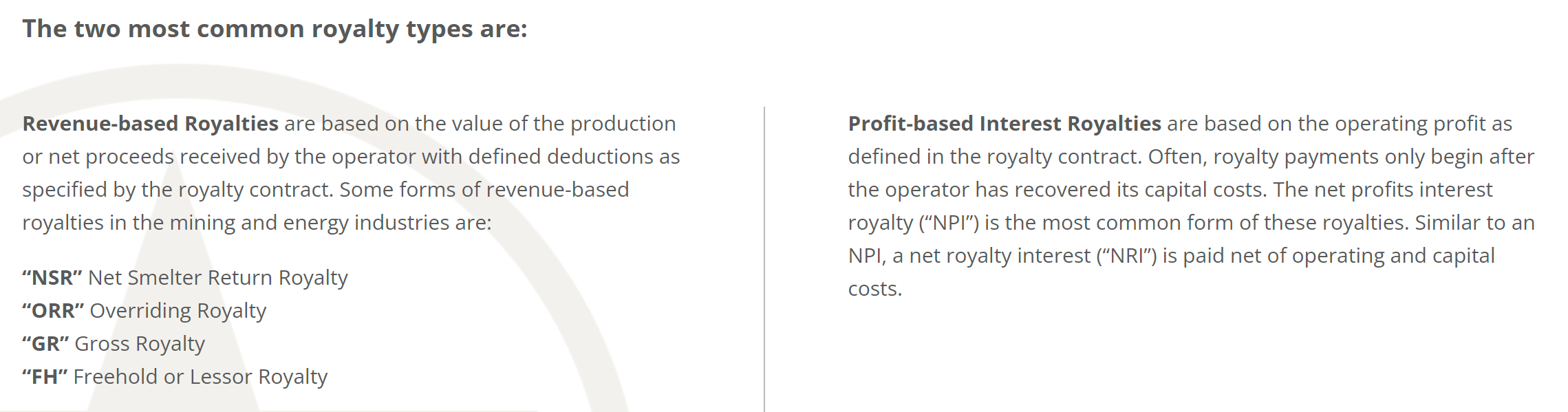

Royalties are usually revenue based and use terms like NSR (Net Smelter Royalty) or GR (Gross Royalty). The visual below explains the most popular types of royalties and how they work.

The visual below is a helpful guide to understanding the economic of different royalties.

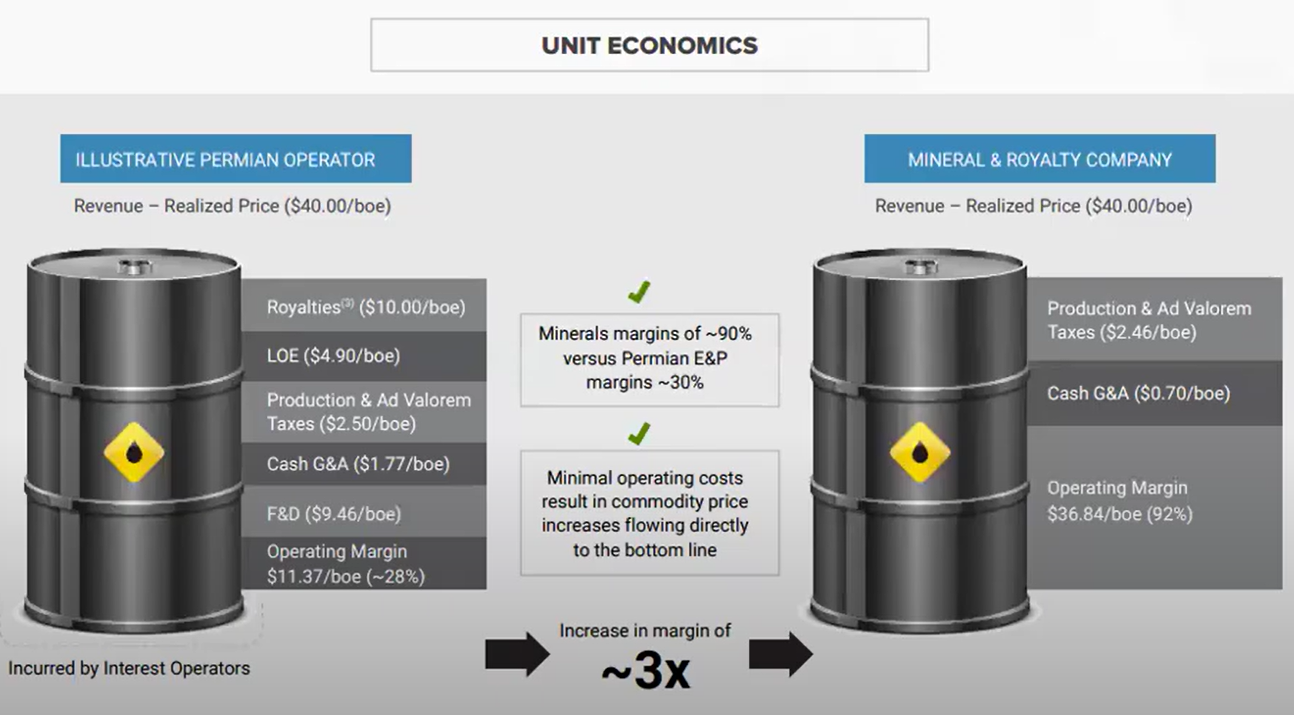

The main difference you should notice is that a royalty has essentially zero production costs. Every $1 of revenue reaches the royalty investor as profit, less taxes.

The only costs you have to worry about is the corporate overhead from paying the salaries of the management team picking the royalties.

Royalty vs Operator Economics (Oil Example)

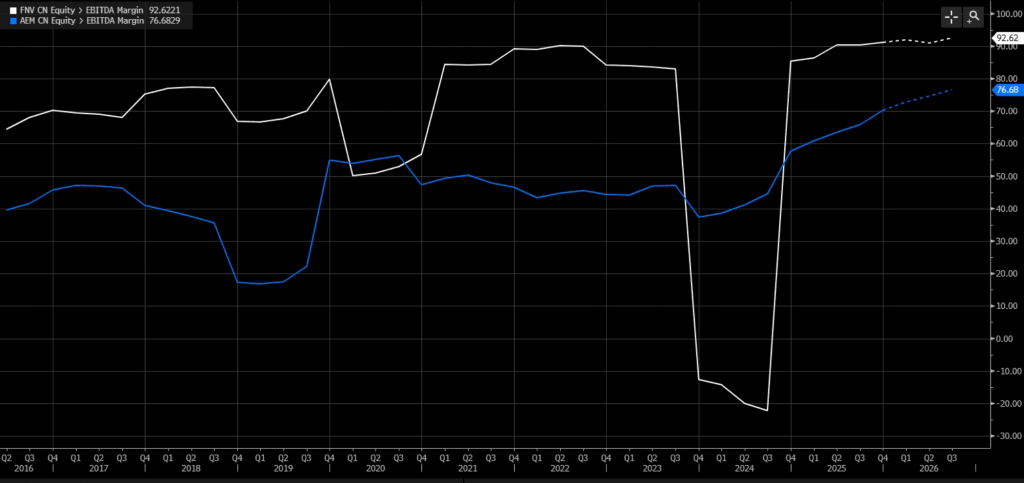

Looking at historical EBITDA margins for a gold miner and a gold royalty company we can see the difference in margins. The royalty generated EBITDA margins between 70%-80% while the miner is half that.

EBITDA Margins Royalty (White) vs Miner (Blue)

Royalties Have Three Key Advantages Over a Pure Mining Stock

Diversification

This is the huge differentiator and the main reason we believe every investor who invests in the mining space should consider owning royalties as well.

Yes we’ve all heard of the mining stock that went up 10 times or more, but what you rarely hear about are the mining stocks that went to zero, and there are a lot of them.

Mining is a risky business, but at a royalty company you own pieces of many different projects picked by a team with significant experience evaluating opportunities.

Royalty companies buy small royalties in many different mines giving investors key diversification by geography, commodity, mine or all three.

If one project dies on the vine, it doesn’t mean an automatic writeoff for your investment.

Mining is by nature a very risky business due to exploration and commodity price uncertainty and diversification is key to staying in the game long enough to find a world class project or discovery.

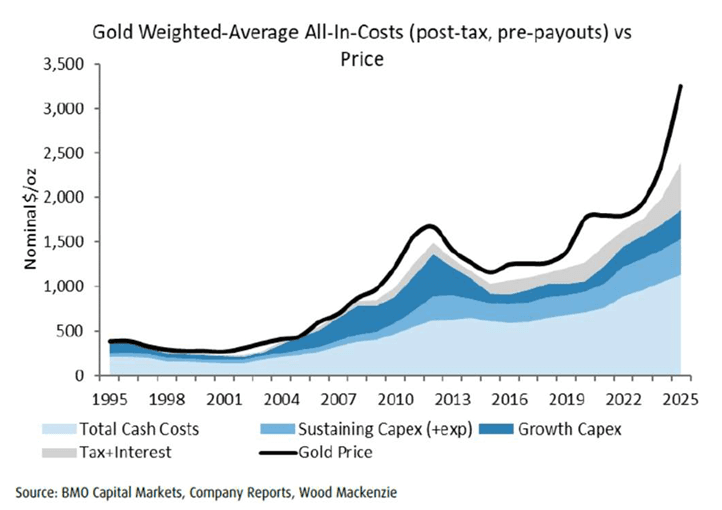

No Exposure to Cost Inflation

Another significant advantage of owning a royalty is that you aren’t exposed to rising operating costs.

Any investor whose been through more than one commodity cycle knows that operating costs are almost always rising, especially when commodity prices are rising as well.

So while the margins on a project end up being squeezed in a bull market, royalty investors are paid out from revenue, capturing 100% of the upside from higher prices.

As long as the company’s margins are high enough to justify keeping the mine in business, royalty investors don’t have to care about operating cost inflation.

This is a huge advantage to owning a royalty.

Mining Costs Rise with Prices Squeezing Producer Margins but not Royalty Payments

Lower Cost of Capital

The diversification benefits of a royalty company feed over into its cost of funding as well.

With less risk that one problem project will sink the company, lenders are willing to offer debt at lower rates.

Debt costs today range between 5%-8.5% depending on the size and operating history of the company which is significantly below debt costs of 10%+ for 102 asset mining companies.

This capital cost arbitrage enhances royalty returns over owning the underlying mining company stock.

Royalty companies still have to compete with public and private markets to fund mining projects which keeps internal rates of return in check somewhat, but with the lack of asset managers in the space, future returns are on the rise.

Royalty Companies Generate Upside Three Ways

The beauty of royalties and miners is they can generate value above and beyond what is priced into the estimated net asset value.

Some royalties even trade at a discount to net asset value which offers additional upside if they can simply execute on the current resource.

We would argue that the company’s trading at a premium to net asset value are simply mispriced vs the true asset value of what they own, meaning good operators can often be bought for a discount before they build a multi-decade track record of success.

As you judge the upside potential of each royalty company, keep in mind the three ways a management team can add value over time.

1: Exploration Success

The value of a royalty increases as more pounds of metal are discovered. While royalty companies aren’t usually the operators of a project, partner drilling and exploration success still accrues to the royalty.

As an example, owning a 1.5% royalty on a property where drilling discovers another 1 million ounces of gold = 1Moz X $2,430 X 1.5% = $36.5M of additional value accruing to the royalty.

Analyst NAV estimates don’t fully account for exploration upside as a general rule making an active drilling campaign very valuable to royalty investors.

2: Accelerating Production

Both the mine operator and the royalty owner come out winners when a mine increases production above what was originally planned.

The main reason ramping up production is so valuable is because of the time value of money. An ounce produced in year 30 all else equal is worth far less to us today than an ounce produced in year 5.

Pulling forward production and cashflow significantly increases the value of a project to royalty holders.

How Exploration Success is Used Depending on Mine Life

In practice a mine with only a 5 year life is unlikely to accelerate production if they find more ounces, they will extend the mine instead. A mine with a 40 year life in contrast, is very likely to accelerate production with drilling success because as we discuss below, pulling forward cashflow that was previously 40 years away is far more valuable than adding a few years to the mine life.

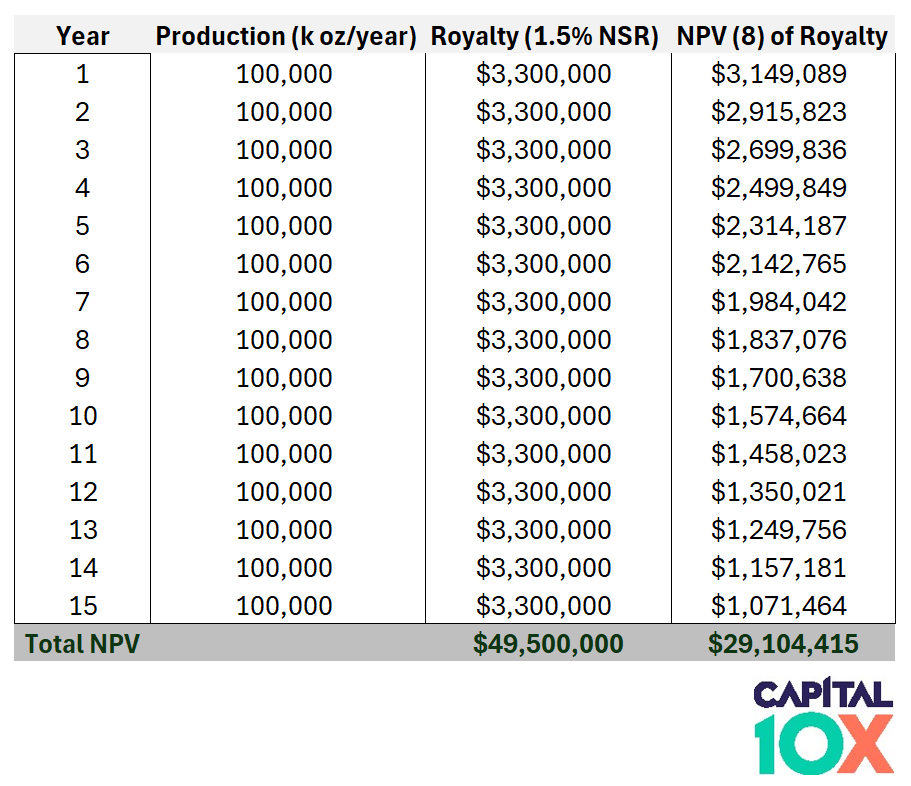

3: Earning the Project’s Cost of Capital

This one is the most straightforward but also least appreciated.

Say a royalty company trades at NAV with an 8% discount rate applied. This means if the portfolio of projects start up on time and produce as expected, you will earn an 8% return over time all else equal.

Over time the gap between the undiscounted net asset value and the NAV with an 8% discount rate closes.

An example will help illustrate. Say we have a mine expected to produce 100,000 oz per year for fifteen years. At $2,200/oz gold the project is worth $29.1 million to us today.

Value of a 100k oz Gold Mine (Year 1)

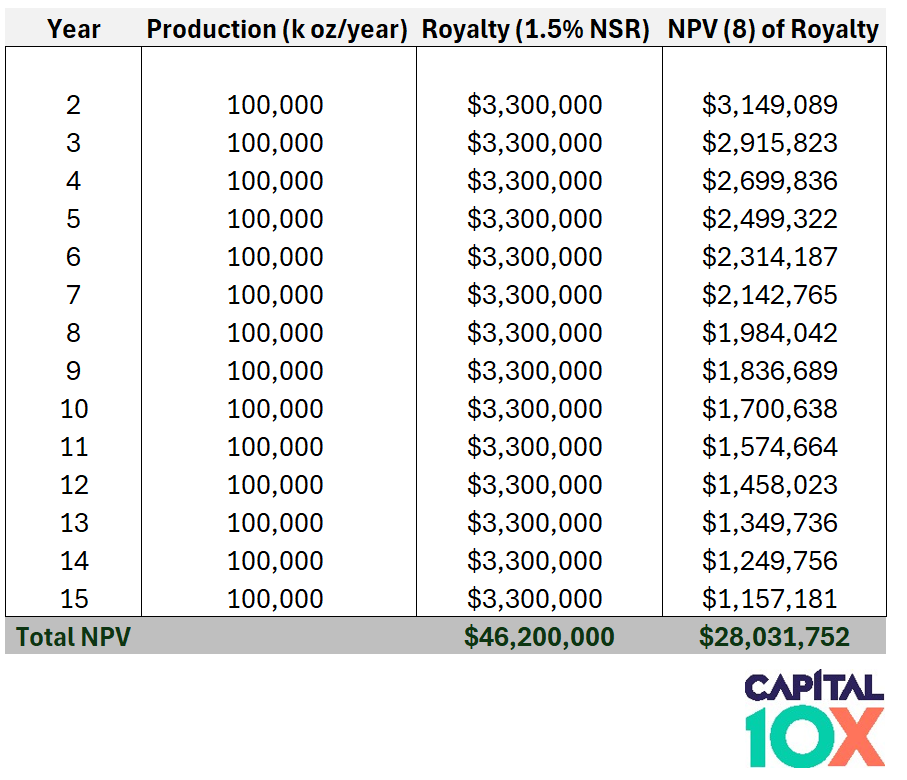

Now lets move forward in time 1 year. The mine has generated $3.3 million of royalties so it should now be worth $29.1M – $3.3M = $25.8M.

But instead the present value is now $28 million, how can this be?

As you move through time the value of future cashflows increase as the NPV approaches the total undiscounted value of the project ($46.2 million).

In this example the NPV of each year gained 8%!

Value of a 100k oz Mine at $2,200 Gold (Year 2)

A mine that can simply produce as planned can generate a significant return for equity owners. But in mining this is often harder than it looks.

You want to find management teams with significant experience building successful mines and working on similar commodities and geological trends if possible.

Three Interesting Royalty Opportunities

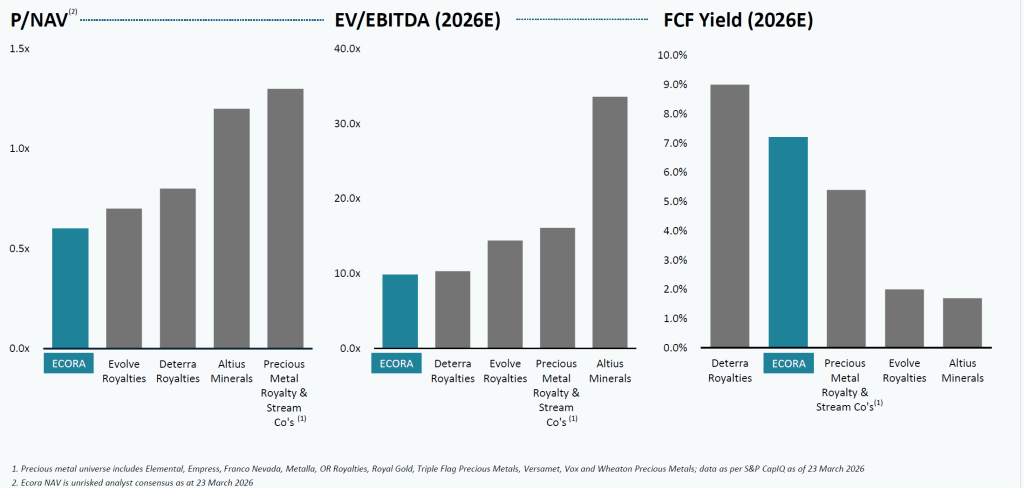

Ecora Royalties (ECOR:TO, LSE:ECOR) Market Cap: C$648 Million

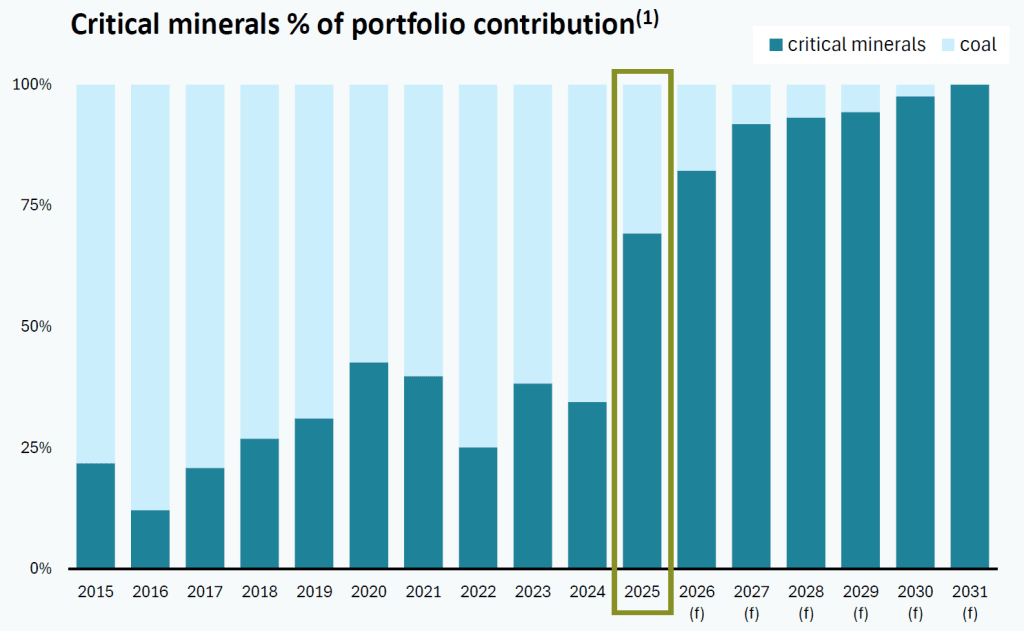

Ecora Royalties is a royalty stock that ticks many of the boxes we discuss in this article.

- Rapidly transitioning its commodity mix to in-demand commodities.

- Ecora’s current share price puts it at ~40% multiple discount to peers, even though the company has best in class expected royalty growth of 12%-18% per year depending if copper prices stay around $5/lb or rise to $7.00-$8.00/lb by the end of the decade.

Given the company plans to continue signing additional royalties, the discount will only grow without a commesurate increase in share price.

Ecora has completely transitioned away from the legacy coal business

Ecora trades at an Iron Ore multiple but will be generating ~90% of cashflow from Copper, Uranium, Cobalt and Nickel by the end of this year. This represents a significant rerating opportunity in addition to typical cashflow and production growth.

Ecora Valuation vs Peers

Royalty income is expected to grow at least 75% from now until 2030 and could be higher if copper prices average above $5.00/lb.

Ecora owns royalties on commodities with strong growth trends, trades at a discount to NAV and most importantly is going through a radical transformation that is currently not priced in by the market.

Franco Nevada (NYSE:FNV) Market Cap: C$68 Billion

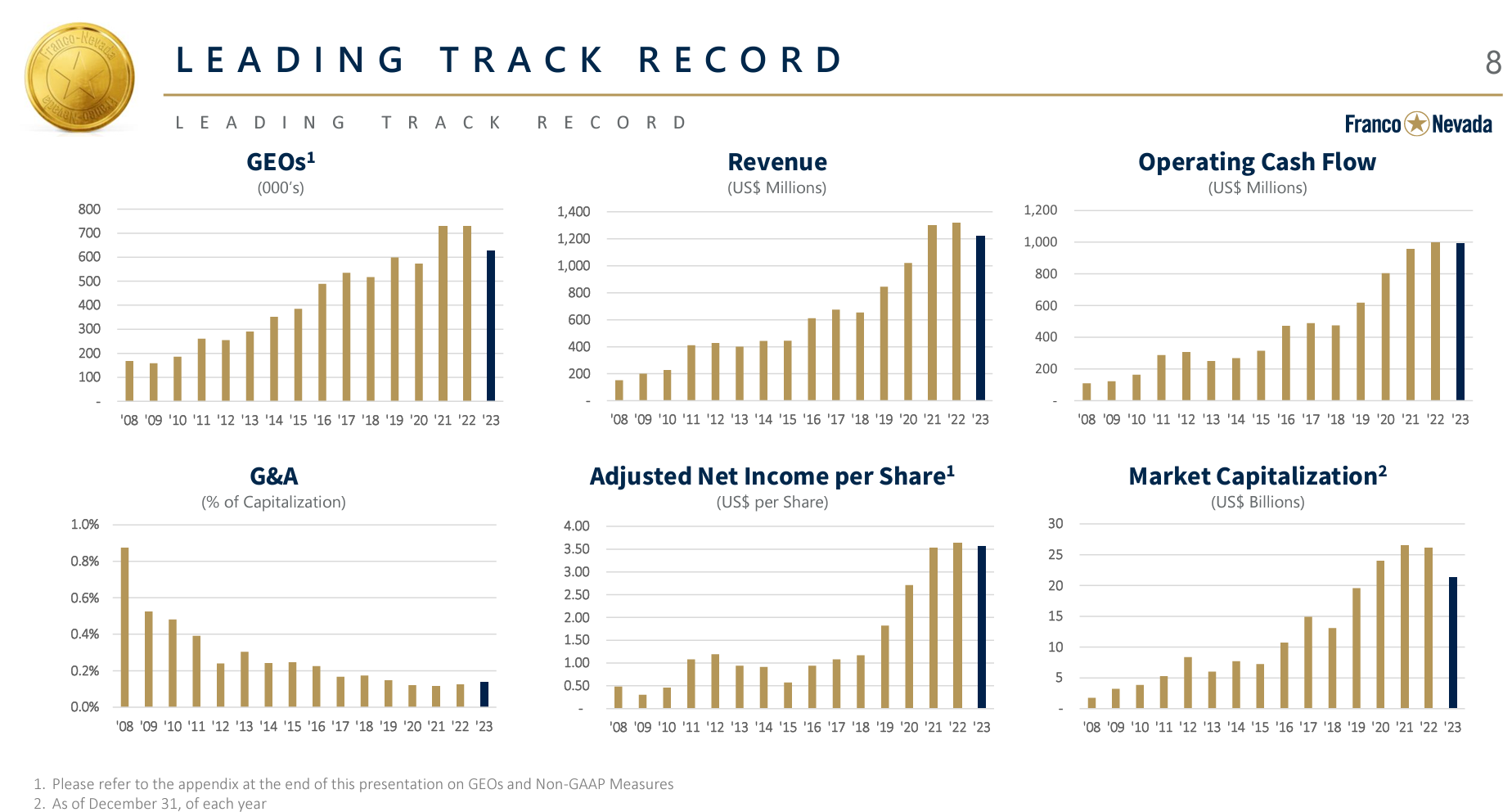

Franco is regarded as potentially the highest quality royalty company globally. The company has grown dividends for 17 years straight and generated a 15% compounded return for investors since IPO.

Management has also been prudent in growing corporate costs slower than revenue leading to a dramatic decline in overhead costs over time.

An Impressive Track Record of Growth and Execution

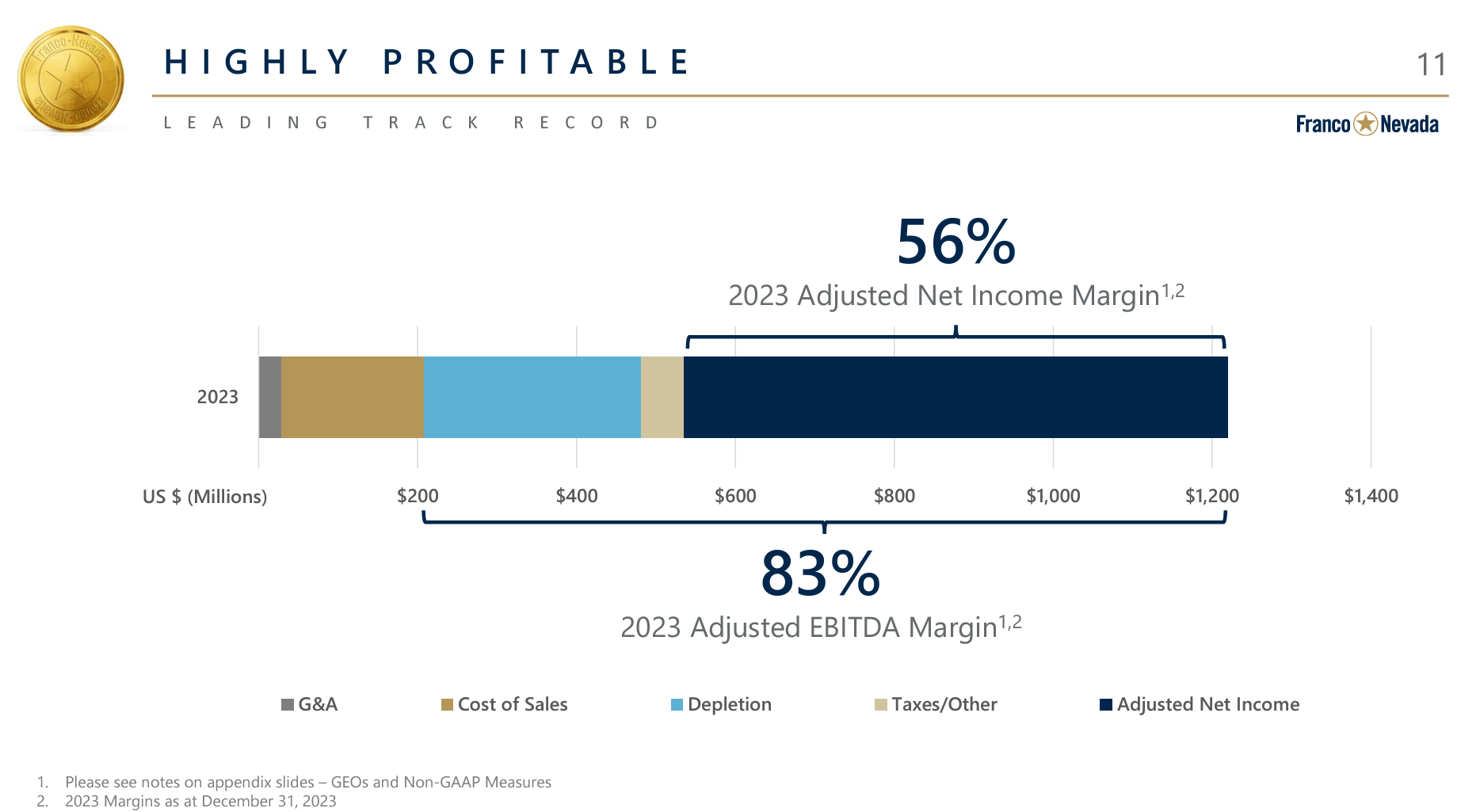

Due to the superior economics of the royalty model, Franco is generating impressive margins of 83% before reinvestment and 56% on a net basis.

Franco Nevada Generates Impressive Margins

Franco is well diversified, owning 431 royalties across the globe with 27% in Production, 10% advancing and 63% exploration stage.

The main reason the company trades at a premium to NAV is a history of generating significantly better returns that what was implied when the royalties were signed.

As we mentioned above, exploration success and stable or accelerating production can generate excess returns for investors and this is exactly what has happened for Franco Nevada shareholders in the past.

With the stock underperforming gold over the past 5 years due to issues at the Cobre Panama royalty, there looks to be a potentially attractive entry point for investors new to the company.

Franco already wrote down the mine by $1.2 billion, so the difficulties are largely priced in leaving upside if political tensions can be resolved.

Franco is yielding 0.6%, close to its all-time low, reflecting record gold prices but still offers a catchup opportunity vs where gold prices trade today.

Franco Nevada Indicated Dividend Yield

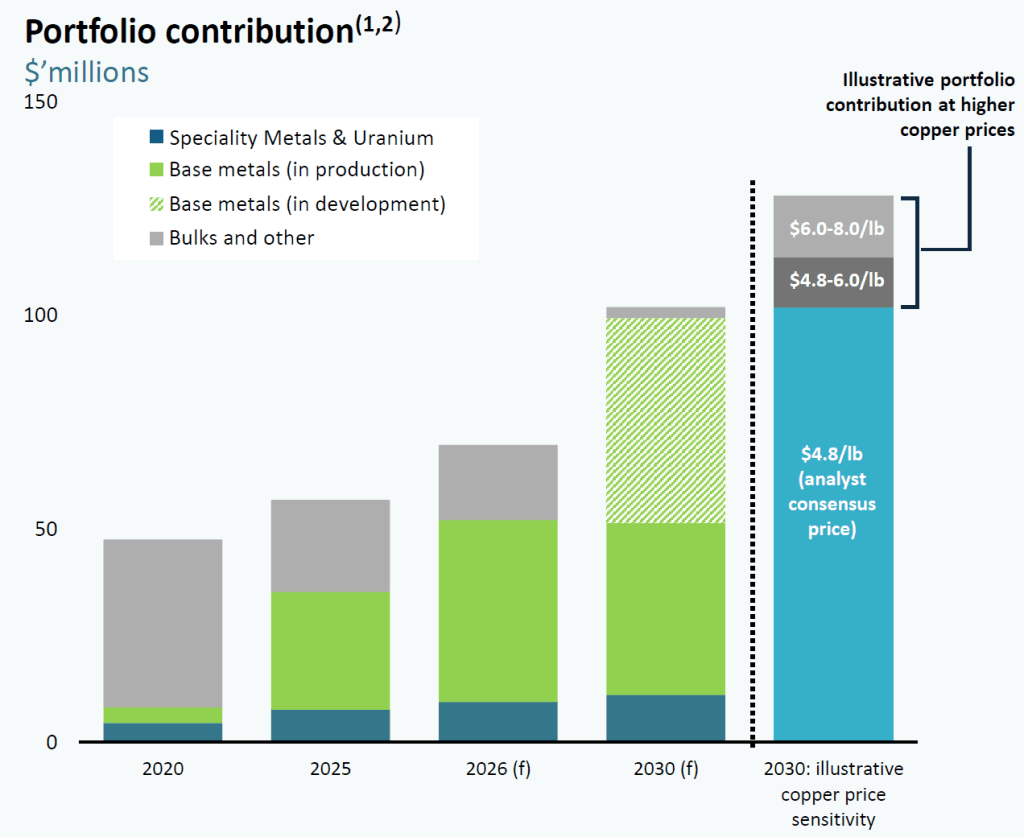

Altius Minerals (NYSE:SAND) Market Cap: C$2.4 Billion

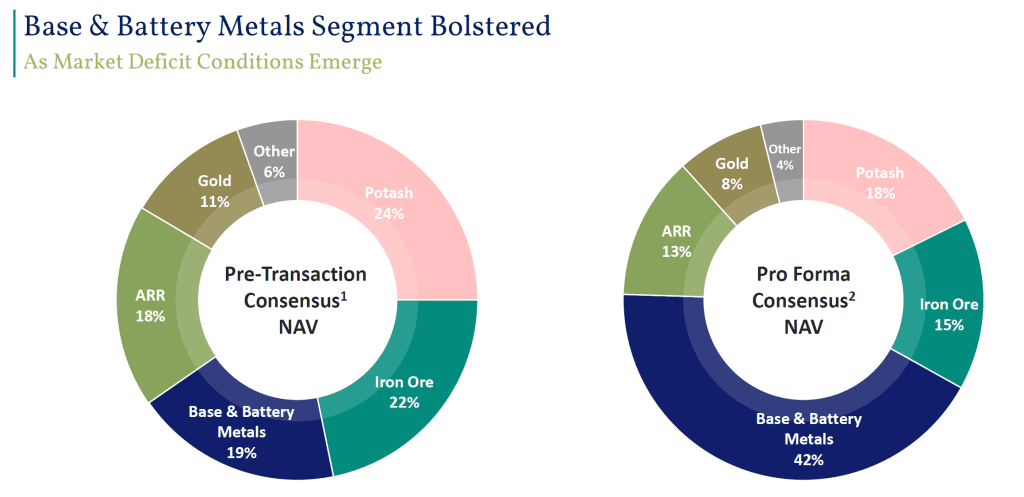

Altius is a St. John’s-based royalty company with 13 paying mineral royalties and a 57%-owned subsidiary, Altius Renewable Royalties (ARR), holding 13 renewable energy royalties across the U.S.

Revenue by Metal

The NAV breakdown tells the story: base and battery metals make up 42% of consensus NAV, potash 18%, iron ore 15%, electricity 13%, and gold 8%. This is not an accident. Copper is the indispensable metal for electrification and faces a structural supply deficit as mine development timelines lengthen.

Potash underpins global food security, and Nutrien and Mosaic — Altius’s royalty counterparties — are guiding for a third consecutive year of rising global demand to 74–77 million tonnes with potential record production from Esterhazy in 2026. The renewable electricity royalties, through ARR’s joint venture Great Bay Renewables, provide contracted cash flows largely insulated from power price volatility via long-term PPAs.

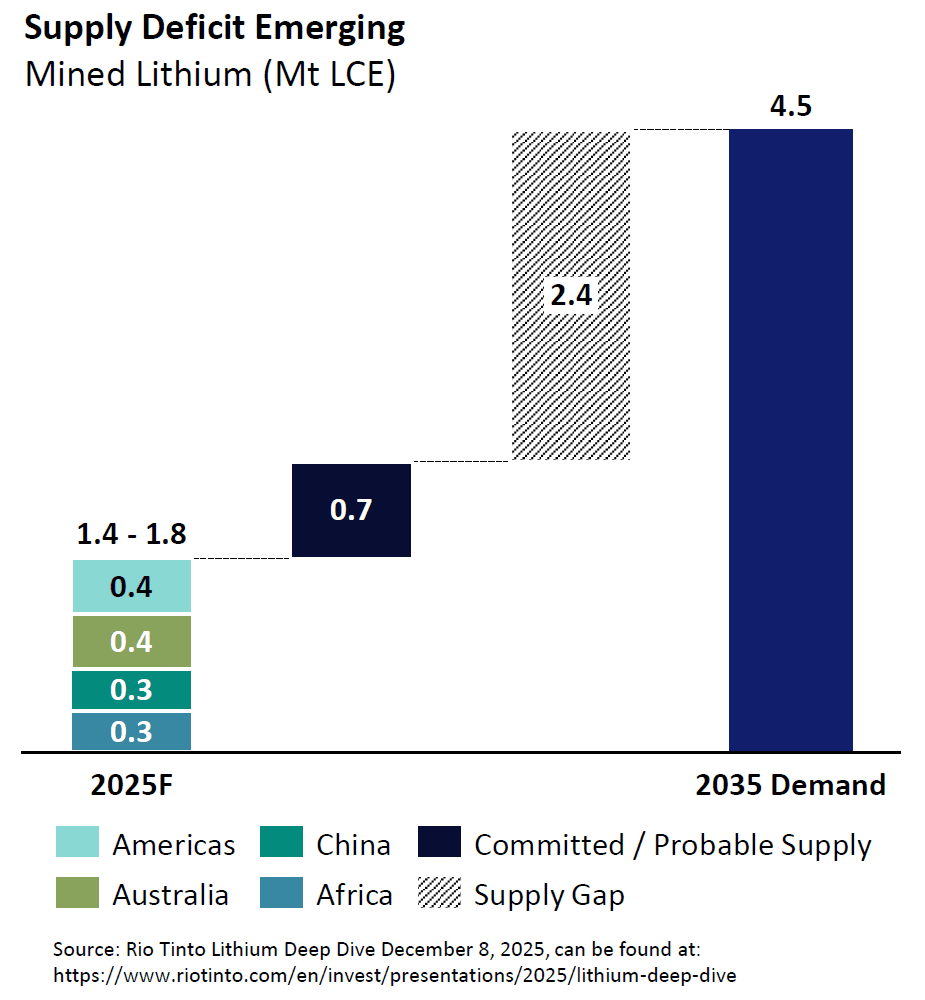

The newest and most exciting addition is lithium. In March 2026, Altius completed its acquisition of Lithium Royalty Corp. (LRC), adding 37 royalties across producing, development, and exploration-stage lithium projects. Four of those royalties cover mines commissioned during the last lithium incentivization cycle, now ramping up.

With lithium demand expected to exceed 1.5 Mt LCE and growing, and prices recovering sharply off their 2024 lows, the timing of this acquisition looks counter-cyclically astute.

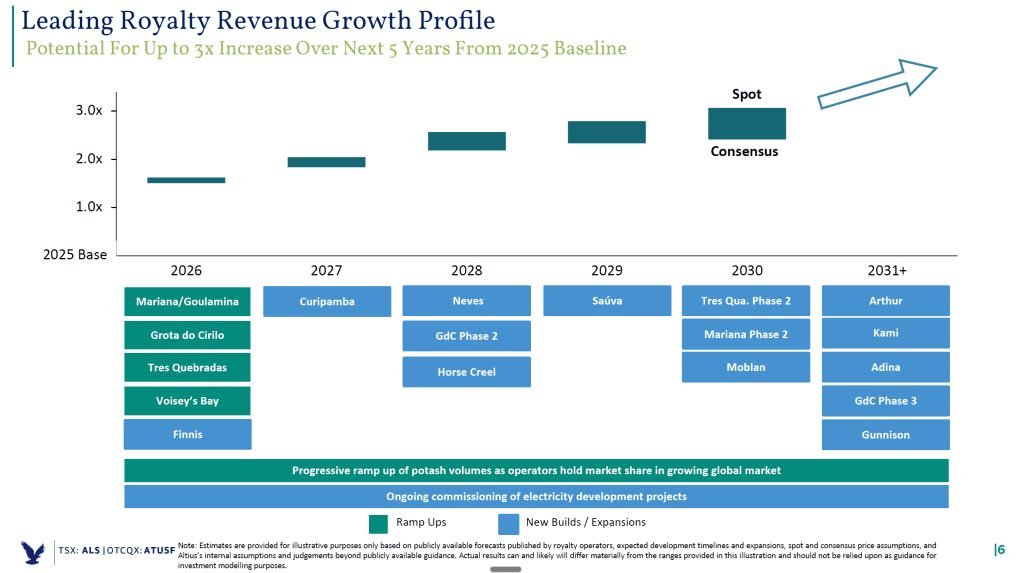

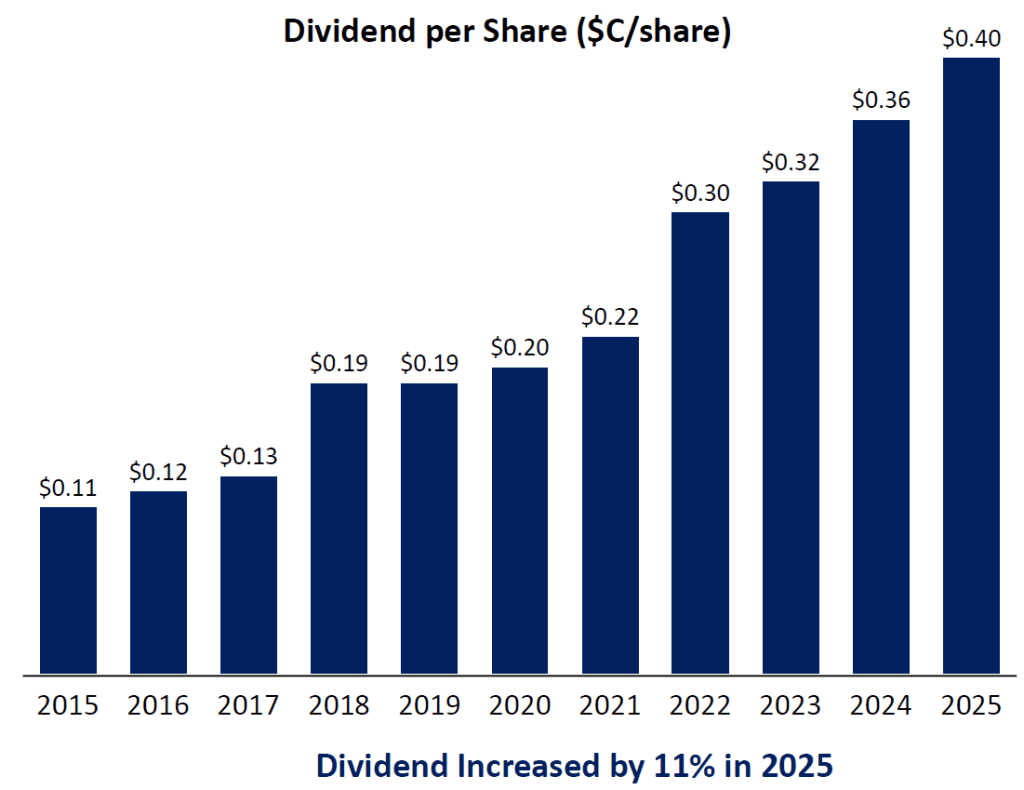

Altius Has a Distinguished History of Dividend and Royalty Growth

Altius stands alone in the royalty universe on forward growth.

Management’s pipeline points to 150–200% cumulative royalty revenue growth by 2031, well ahead of Ecora’s 75%-100% expected growth and the low-to-mid single-digit compound growth typical of the precious metal peer group.

There is no other diversified royalty company with such a long track record of operations and dividend payments offering such rapid growth in the market today.

That exceptional growth profile justifies the meaningful valuation premium. Altius has earned its valuation based on its long history of profitable growth and shareholder payouts. The dividend per share has grown from C$0.11 in 2015 to C$0.40 in 2025, a 264% increase over a decade, with a further 11% raise in 2025 alone. That unbroken track record of dividend growth, backed by a 28-year history of per-share value creation, gives the 36x EV/EBITDA multiple a credibility that pure growth-stage royalty companies simply cannot claim.

A Long History of Dividend Growth

You Can’t Afford Not to Own Royalty Companies

Any mining investor, without millions to invest like Eric Sprott and others, who doesn’t own a barbelled portfolio of mining companies and royalties is signaling a significant lack of experience.

At this point the royalty model has been tried, tested and emerged victorious. The lack of exposure to cost inflation and protection through asset diversification removes the two main risks that usually sink a portfolio owning pure play miners.

Now with asset managers, a major competitor, shrinking away from the market, royalty company’s are emerging as a critical source of project funding for miners, likely leading to better terms on deals and better future returns for royalty investors.