Ecora Royalties PLC (LSE/TSX: ECOR) announces full year results for the year ended 31 December 2025. The Company will publish its audited 2025 Annual Report and Accounts later today, which will be available on the Group’s website at www.ecoraroyalties.com and on SEDAR.

Ecora Royalties PLC (LSE/TSX: ECOR) announces full year results for the year ended 31 December 2025. The Company will publish its audited 2025 Annual Report and Accounts later today, which will be available on the Group’s website at www.ecoraroyalties.com and on

Ecora is a leading critical minerals focused royalty and streaming company. Copper is at the core of the portfolio which also includes other commodities linked to the trend of electrification, energy transition, infrastructure renewal and urbanisation, digital infrastructure, robotics and energy security.

Marc Bishop Lafleche, Chief Executive Officer, commented:

“2025 was a landmark year for Ecora. Our critical minerals royalties and streams delivered record portfolio contribution representing the first time in the Group’s history where the majority of the Group’s portfolio contribution was derived from critical minerals.

“Project’s underlying Ecora’s development stage portfolio saw a number of meaningful advances during 2025, with our operator partners targeting further derisking events in the upcoming twelve months which will move these projects closer to production, underpinning a key part of Ecora’s organic growth profile during the remainder of the decade and beyond.

“Ecora has delivered strong deleveraging post the acquisition of the Mimbula copper stream, which is expected to continue in 2026. Ecora retains the financial flexibility to continue to further diversify its portfolio, with a primary focus on acquiring producing or advanced stage near-production royalties or streams, to complement Ecora’s existing growth portfolio.”

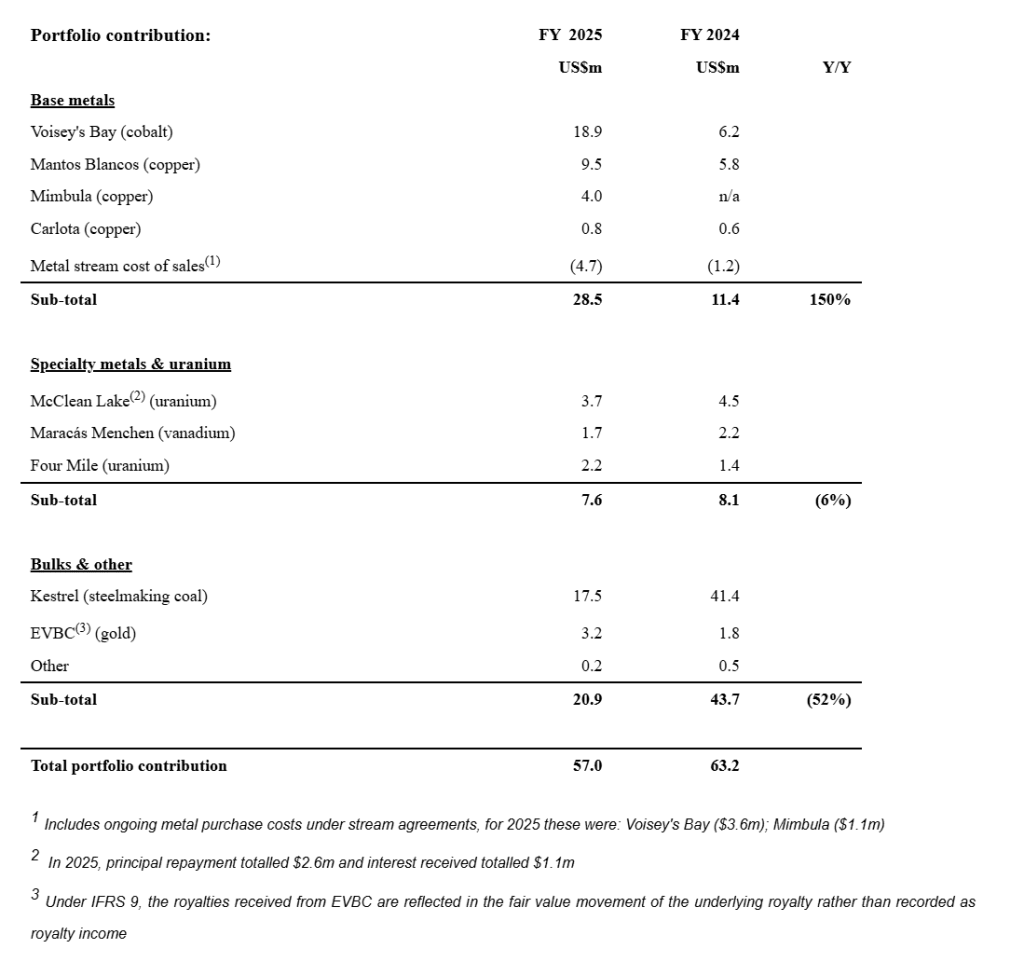

Financial Highlights:

· $57.0m portfolio contribution for the year ended 31 December 2025 (2024: $63.2m) with significant increase in contribution from base metals royalties largely offsetting reduction in Kestrel steelmaking coal contribution

· Royalty and metal stream-related revenue of $55.9m (2024: $59.6m)

· Profit after tax of $22.2m (2024: loss of $9.8m)

· The latest Voisey’s Bay mine plan extends production by four years to 2044 and accelerates near-term volumes, as a result, the Group has recognised an impairment reversal of $14.1m and a related deferred tax credit of $9.8m relating to carry forward losses which are now expected to be utilised

· Adjusted earnings of $22.1m (2024: $28.9m) and adjusted earnings per share of 8.86c (2024: 11.43c)

· Free cash flow of $27.4m (2024: $22.1m), a 21% increase

· Strong deleveraging post the $50.0m Mimbula stream acquisition with net debt as at 31 December 2025 of $85.5m (31 Dec 2024: $82.3m), significantly below the peak of $124.6m during Q2 2025

· Final dividend of 1.4c per share in line with policy, bringing the total dividend for the year to 2.0c per share (2024: 2.81c per share)

Base Metals

· Base metals portfolio contribution of $28.5m, up 150% (2024: $11.4m) and representing 50% of Group portfolio contribution, driven by:

o Strong production ramp-up at Voisey’s Bay, which generated a net portfolio contribution of $15.3m (2024: $5.0m) from 448t of attributable cobalt (2024: 210t) at an average realised price of $19.11/lb (2024: $13.34/lb)

o Record year portfolio contribution from Mantos Blancos of $9.5m (2024: $5.8m)

o Acquisition of a copper stream over the Mimbula mine in March 2025, which generated portfolio contribution net of metal purchase costs of $2.9m in 2025 (2024: n/a)

Specialty metals & uranium

· Specialty metals portfolio contribution of $7.6m (2024: $8.1m) representing 13% of the Group’s portfolio contribution:

o Toll milling rate at McClean Lake Mill stepped down in 2025 following the processing of an agreed volume of uranium, leading to a portfolio contribution of $3.7m (2024: $4.5m)

Bulks & other

· Bulks and other portfolio contribution of $20.9m (2024: $43.7m) represented 37% of the Group’s portfolio contribution:

o Kestrel steelmaking coal royalty generated $17.5m from 2.2mt of sales from the Group’s private royalty area, down vs. 2024 due to a lower average realised sale price of $143/t (2024: $223/t)

· Sold a non-core royalty over the development stage Dugbe Gold Project in Liberia for a $16.5m upfront cash payment and contingent consideration of up to $3.5m

Outlook

· Ecora’s key commodity exposures performed strongly in early 2026. The conflict in Iran has resulted in market and commodity price volatility, however the long-term commodity price outlook, in particular copper, continues to be underpinned by strong supply/demand fundamentals

· Volume growth in base metals royalties and streams expected to continue to offset a reduction in volumes from Kestrel associated with mining increasingly moving outside the Group’s private royalty area

· Series of value catalysts during the next twelve months with operator partners targeting a number of key project development milestones, including:

o Santo Domingo: Final investment decision

o Mantos Blancos: Phase II study mid-2026

o Phalaborwa: Publication of DFS

o Nifty: Restart of cathode operations, DFS on restart of mining operation

Analyst and investor presentation and call

A live webcast of the presentation including Q&A will be held today at 2:00 pm GMT for investors and analysts and will be available via our website at www.ecoraroyalties.com.

Please join the event 5-10 minutes prior to the scheduled start time.

This will be available for playback after the event.